International Bill of Exchange (IBOE)

My own introduction of what it is.

10/3/20257 min read

Introduction

An International Bill of Exchange is a widely used financial instrument in global trade. It facilitates payments between parties in different countries, offering security and flexibility in settling international transactions. This document provides a thorough exploration of the concept, its legal framework, practical applications, and guidance on how to use it effectively.

What Is an International Bill of Exchange?

An International Bill of Exchange is a written, unconditional order from one party (the drawer) to another (the drawee), directing the drawee to pay a specified sum to a third party (the payee) either immediately (at sight) or at a future date. Unlike domestic bills, international bills of exchange are governed by international conventions, such as the Geneva Convention of 1930 and the United Nations Convention on International Bills of Exchange and International Promissory Notes (UNCITRAL Convention).

Key Features

Unconditional Order: The bill must not be contingent on any condition.

Written Document: It must be in writing and clearly specify the amount, parties involved, and payment terms.

Negotiability: Bills of exchange are negotiable instruments, meaning they can be endorsed and transferred to other parties.

International Application: Used for transactions between parties in different countries, subject to international laws and conventions.

Specified Payment Date: Payment can be at sight (on presentation) or at a fixed/future date.

Legal Framework

Indian Negotiable Instruments Act 1881 in India:

Negotiable instruments can be anything that has a monetary value and is transferable. It enlists cheques, exchange bills, and promissory notes but excludes hundis, the original bill of exchange used in ancient India.

UCC (Uniform Commercial Code) in the United States:

The UCC, established in the 1950s, governs commercial transactions and trade practices across all U.S. states. It provides regulations for using bills of exchange, ensuring uniformity in business dealings, including rules on issuance, negotiation, and enforcement of these financial instruments.

Bills of Exchange Act in the United Kingdom:

The Bills of Exchange Act 1882, along with subsequent amendments, provides the legal framework for using bills of exchange in the UK. It outlines the rights and obligations of parties involved in the exchange, governing aspects such as presentment, acceptance, and dishonor, and ensuring the smooth functioning of these financial instruments within the British legal system.

Other International Regulations:

Apart from country-specific regulations, international bodies like the International Chamber of Commerce (ICC) and the United Nations Commission on International Trade Law (UNCITRAL) have developed frameworks and guidelines for international trade, including provisions for bills of exchange. These frameworks aim to harmonize laws and practices concerning bills of exchange across different jurisdictions, facilitating smoother global trade transactions.

International bills of exchange are primarily regulated by:

Geneva Convention (1930):

Establishes uniform laws for bills of exchange and promissory notes in signatory countries.

UNCITRAL Convention (1988):

Provides rules for international bills and promissory notes, facilitating harmonized global usage.

Local Laws:

Each country may have additional regulations affecting the use and enforcement of bills of exchange.

Structure and Components

A typical international bill of exchange includes the following elements:

Date and place of issue

Name of the drawer

Unconditional order to pay

Name of the drawee

Amount to be paid (in specified currency)

Date and place of payment

Name of the payee

Signature of the drawer

How to Use an International Bill of Exchange

Drafting the Bill:

Ensure all required components are included and comply with international conventions.

Use clear, unambiguous language.

Presenting the Bill:

The drawer presents the bill to the drawee for acceptance (agreeing to pay).

Once accepted, the drawee becomes legally obligated to pay the specified amount to the payee.

Endorsement and Transfer:

The payee or holder can endorse (sign over) the bill to another party, making it a negotiable instrument.

Payment:

On the due date or upon presentation (for sight bills), the drawee must pay the holder of the bill.

Payment is typically made through banking channels, ensuring proper documentation and record-keeping.

Dishonor and Recourse:

If the drawee fails to pay, the holder can seek recourse against previous endorsers or the drawer.

Legal proceedings may be initiated, depending on the jurisdictions involved.

Types of International Bills of Exchange

Promissory Note:

This is a two-party instrument where one party makes an unconditional promise in writing to pay a determined sum of money to the other party.

Sight Bill:

A sight bill is payable immediately upon presentation to the drawee for payment or acceptance. The payee can demand payment on bill presentation.

Time Bill:

A time bill specifies a definite period after it becomes payable. It allows the drawee a specific period, usually from days to months, to make the payment.

Advantages of Using International Bills of Exchange

Security: Provides legal protection and a formal payment method.

Negotiability: Easily transferable, facilitating trade finance.

Flexibility: Can be used for deferred payments, enabling better cash flow management.

International Acceptance: Recognized globally, making cross-border transactions more efficient.

Risks and Considerations

Jurisdictional Differences: Laws vary by country, so it's essential to understand local regulations.

Credit Risk: If the drawee defaults, recovery may be complex, especially across borders.

Fraud: As with any financial instrument, there is a risk of forgery or fraudulent endorsement.

Exchange Rate Risk: Currency fluctuations can affect the value of payments.

Regulatory Compliance

Regulatory Compliance is essential when handling bills of exchange formats involving stringent legal requirements and documentation practices.

Legal Requirements:

Comply with the legal provisions outlined in the relevant bills of exchange acts and international trade regulations, ensuring the validity and enforceability of the financial instrument.

Documentation and Record-Keeping:

Accurate records of all bill-related transactions, including issuance, acceptance, and payments, are important to maintain to facilitate transparency and audit trails.

Reporting Obligations:

Fulfill reporting obligations as mandated by regulatory authorities, providing timely and accurate information related to bill transactions and financial dealings.

Non-Compliance:

Non-compliance can lead to legal penalties, financial liabilities, and reputational damage, jeopardizing business relationships and impeding future transactions.

Best Practices

Consult with legal and financial experts familiar with international trade laws.

Use standardized forms and language as per international conventions.

Verify the identities and creditworthiness of all parties involved.

Keep thorough records of all transactions and endorsements.

Use secure banking channels for payment and presentation.

Conclusion

International Bills of Exchange are powerful tools for facilitating global trade and finance. By understanding their structure, legal framework, and practical usage, businesses and individuals can leverage them to streamline cross-border payments, manage risk, and enhance commercial relationships. Proper due diligence and adherence to best practices are essential for maximizing their benefits and minimizing potential challenges.

Warnings

IBOE (International Bills of Exchange) related scams have become increasingly sophisticated, often targeting businesses engaged in cross-border transactions. Fraudsters may attempt to present counterfeit bills, manipulate documentation, or impersonate legitimate parties to extract payments or sensitive information. Common schemes include presenting forged bills for acceptance, altering payee details, or intercepting communications to redirect funds. These scams can result in significant financial losses and reputational damage if not detected promptly.

Red Flags to Watch Out For:

Unexpected requests to alter payment instructions or beneficiary details at the last minute.

Pressure to proceed with transactions urgently, bypassing standard verification procedures.

Discrepancies in documentation, such as mismatched signatures, inconsistent letterheads, or poor-quality copies.

Lack of verifiable contact information or reluctance to provide company credentials.

Requests to use unfamiliar or unregulated banking channels for payment or presentation.

Unsolicited offers involving unusually favourable terms or large sums of money.

Communication from generic email addresses rather than official company domains.

Staying vigilant and maintaining robust verification processes can help mitigate the risk of falling victim to IBOE-related scams.

Case Study

Step By Step Scenario

Creation and Initial Acceptance

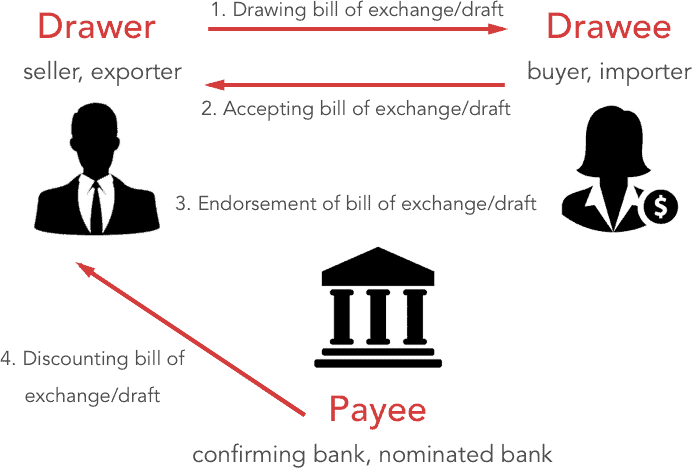

The journey of an IBOE begins with its creation by the exporter, also known as the drawer.

The exporter drafts the IBOE, ordering the importer (the buyer) to pay a specific amount.

(This document contains details such as Amount Due, Payment Date, Payee information and Instructions for Acceptance.)

Upon receiving the IBOE, the importer (now the drawee) reviews its terms. If agreeable, the importer formally accepts the IBOE by signing it. This act of acceptance establishes a secondary legal obligation on the importer, thereby granting the exporter (drawer) a legally binding right to receive payment on the agreed date.

Transfer to a Negotiable Instrument

With the accepted IBOE in hand, the exporter can choose to negotiate it with a bank. This negotiation typically involves selling the IBOE to the bank at a discounted rate, with the bank assuming responsibility for payment at maturity. The bank then becomes the acceptor, taking on the obligation to pay the payee when the bill matures.

Negotiating the IBOE with a bank benefits the exporter by providing quicker access to funds and mitigating risks associated with waiting for the importer’s payment. The bank assesses the creditworthiness of the importer and may apply a discount, which acts as a form of interest for assuming the risk.

Bank's Role in Monetisation

The bank plays a pivotal role in monetising the IBOE. The process begins with the bank’s thorough assessment of both the IBOE and the financial standing of the importer. This involves evaluating factors such as the importer’s credit history, financial statements, and overall economic outlook to determine whether to accept the IBOE.

Once accepted, the bank effectively guarantees payment to the payee on the specified date, providing an added layer of security that makes the IBOE easier to monetise. If the IBOE has been negotiated, the bank pays the exporter a discounted sum, reflecting both the risk assumed and the cost of providing the service.

Receiving the discounted value allows the exporter to convert the future value of the IBOE into immediate cash, although this amount is less than the full face value. The difference—the discount—serves as the bank’s profit for providing financing.

At maturity, the importer instructs their bank to pay the exporter, initiating the payment process. The importer's bank (drawee bank) then transfers the funds to the payee's bank (acceptor bank) according to the terms set out in the IBOE. Often, a network of banks operating across different countries facilitates the flow of funds and ensures the payment obligation is fulfilled.

Leveraging the IBOE's Creditworthiness

Banks do not accept IBOEs based solely on their face value; instead, they rely heavily on the creditworthiness of the importer (drawee) to determine the likelihood of repayment. For transactions deemed high risk, credit insurance or guarantees may be obtained to safeguard the exporter in case the importer defaults.

In some cases, the exporter may pledge collateral, such as inventory or accounts receivable, to the bank to secure the IBOE. This reduces the risk to the bank and facilitates easier monetisation.

Converting Proceeds into Usable Funds

Once the exporter or bank receives the proceeds from the IBOE—be it the face value or the discounted amount—these funds can be converted into cash through several mechanisms:

Currency conversion, if the funds are received in a foreign currency, to the exporter’s local currency

Depositing the funds into the exporter’s bank account

Investing the proceeds in other business ventures

Using the funds as collateral for refinancing, such as obtaining a loan for expansion or working capital

Summary of the Monetisation Process

Establishing the IBOE: Creation of a written order for payment

Bank Acceptance: A bank guarantees payment at maturity, enhancing the IBOE’s creditworthiness

Discounting (optional): The exporter receives a discounted sum ahead of maturity

Collection and Payment: Funds are transferred through a network of banks to fulfil the payment obligation

Utilising Proceeds: Conversion of received funds into cash for business operations, investment, or refinancing.

Key Benefits of Monetising IBOEs

Improved cash flow, enabling exporters to receive funds more quickly than waiting for direct payment from the importer

Reduced risk due to the involvement of banks and their guarantees

Increased facilitation of international trade through a reliable payment mechanism

Access to financing, as the IBOE can serve as collateral for loans and credit arrangements

All Rights Reserved

Co. Reg. No. 201733624H

Our mission

We strive towards forging relationships that creates value not only to the corporates, but also bearing in mind the community that will benefit from our values.

Our vision

To forge strong ties, enabling the "humanitarian" hearts ahead.