GPI Fully Automatic

Explains in detail how GPI Works

10/3/20252 min read

GPI Fully Automatic Transaction

GPI stands for Global Payments Innovation. A GPI Fully Automatic Transaction is a streamlined, automated process for international payments that aims to improve speed, transparency, and cost-efficiency compared to traditional correspondent banking methods. Essentially, it eliminates the manual steps and delays inherent in legacy cross-border payment systems.

Here's a breakdown of what it is and what it entails:

The Problem GPI Solves:

Traditionally, international payments involved a complex chain of correspondent banks. These banks act as intermediaries to facilitate funds transfers between different countries. This process is often:

* Slow: Transfers can take several days (often 3-5 business days or even longer).

* Expensive: Numerous fees are charged at each intermediary bank.

* Lack of Transparency: It's often difficult to track the status of a transaction.

* Manual Processes: Correspondent banking involves a lot of paperwork, manual verification, and reconciliation.

How GPI Works (Fully Automatic Transactions):

GPI aims to eliminate many of these inefficiencies by:

Direct Connectivity: GPI provides direct connectivity between banks. This allows for a more efficient flow of information and reduces the need for intermediary banks.

Automated Data Exchange: Transaction data is transmitted electronically, eliminating the need for manual data entry. It reduces human error and speeds up the process. Automated reconciliation ensures accuracy.

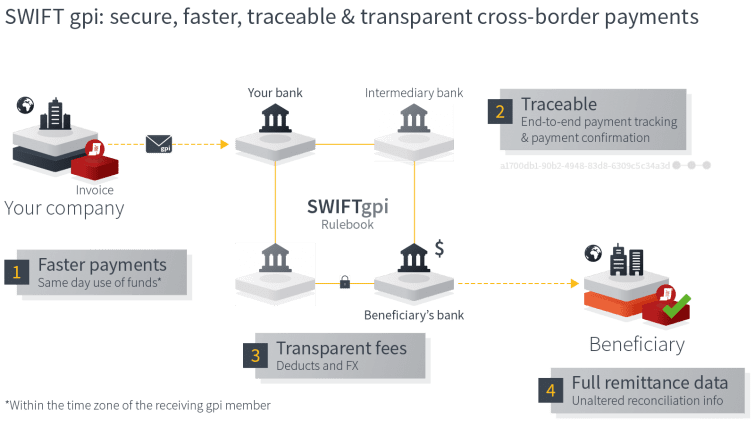

Standardized Protocols: GPI adheres to standardized communication protocols (like SWIFT gpi) ensuring interoperability between banks.

Real-time Tracking & Visibility: Offers end-to-end transaction tracking, giving payers and payees real-time visibility into the status of their transactions.

Faster Settlement: Aiming for faster settlement times, often reducing transfers to just a few business hours (sometimes even intraday).

Key Features & Benefits of GPI Fully Automatic Transactions:

Speed: Faster transaction settlement – often within a few business hours.

Transparency: Real-time tracking and transaction visibility.

Cost Reduction: Reduced fees compared to traditional correspondent banking. (Although some fees may still exist)

Efficiency: Automated processes reduce manual effort and errors.

Improved Customer Experience: Faster transfers and better visibility enhance customer satisfaction.

Scalability: Designed to handle large volumes of transactions.

Compliance: GPI helps banks meet regulatory requirements for international payments.

How a GPI transaction looks (Simplified Example):

Initiation: A payer instructs their bank to make an international payment to a payee's bank.

Data Transmission: The payer's bank transmits the transaction data electronically using GPI's standardized protocols.

Routing: The transaction is routed through GPI's network of connected banks to the payee's bank.

Validation: Automated validation checks the transaction data for accuracy.

Settlement: Funds are settled between the payer's and payee's banks.

Notification: The payer and payee receive notifications about the transaction status.

Who Uses GPI Fully Automatic Transactions?

* Corporations: Companies that frequently make international payments for suppliers, employees, and other expenses.

* Financial Institutions: Banks that want to streamline their cross-border payment processes.

* Businesses: Anyone involved in international trade or remittances.

SWIFT gpi & GPI:

It’s important to understand that GPI is a framework built on top of SWIFT's messaging standard, SWIFT gpi. SWIFT gpi is the technical backbone that enables GPI functionality. SWIFT provides the standardized communication protocol, and banks use GPI to implement more efficient payment workflows using that protocol.

All Rights Reserved

Co. Reg. No. 201733624H

Our mission

We strive towards forging relationships that creates value not only to the corporates, but also bearing in mind the community that will benefit from our values.

Our vision

To forge strong ties, enabling the "humanitarian" hearts ahead.